- Global smartphone SoC shipments declined 8% YoY in Q1 2026, impacted by the ongoing memory crunch.

- Premium smartphones remained relatively resilient with price increases passed on to consumers, while the entry-level segment started adopting older-generation SoCs.

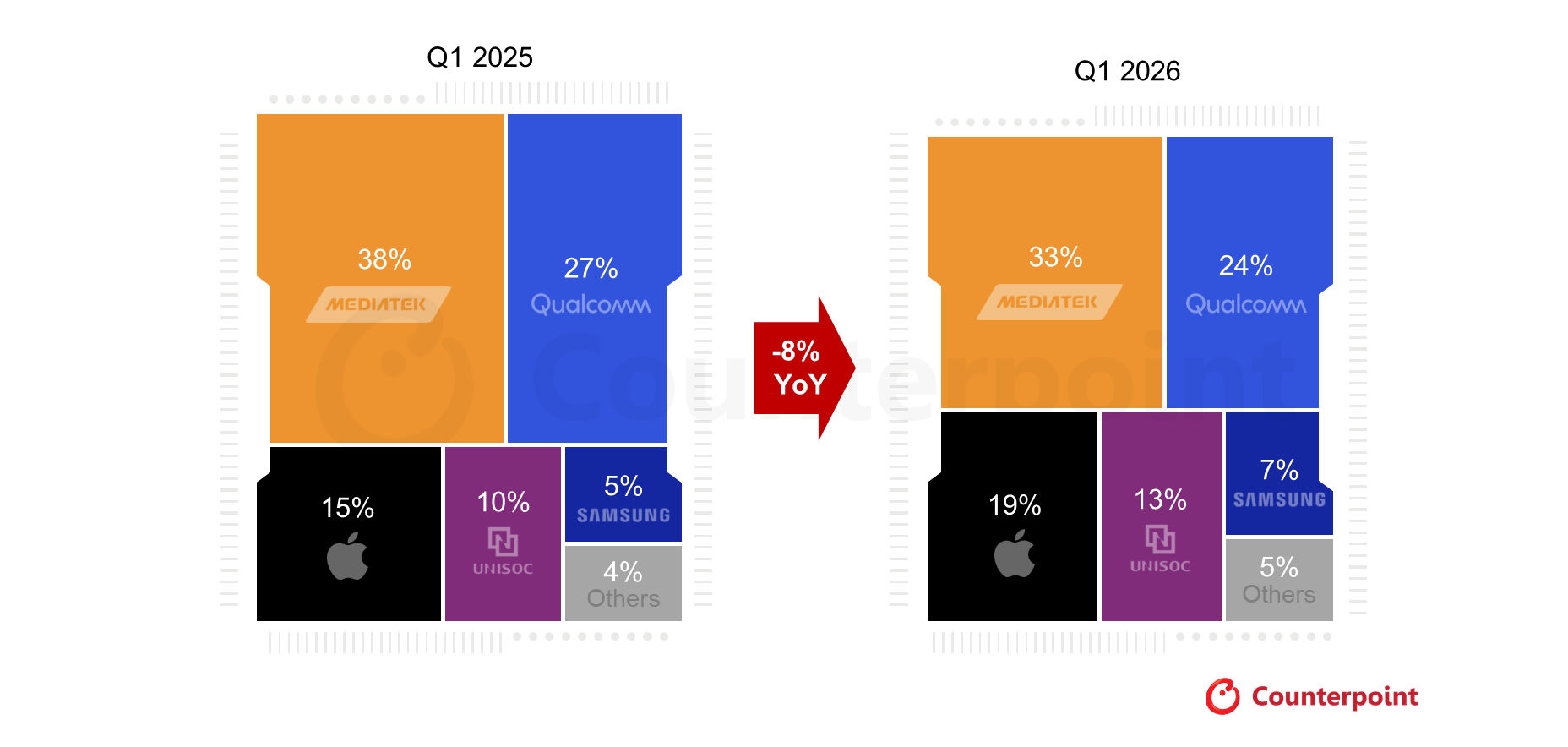

- Qualcomm and MediaTek saw double-digit shipment declines, while Apple, Samsung and Google posted growth, supported by stronger supply chain integration.

- UNISOC gained share in the low-end 4G and entry-level 5G segments, driven by increasing adoption at Chinese OEMs like Redmi and Pocophone.

- Rising memory prices and geopolitical tensions are pressuring markets, driving double-digit declines in Q2 SoC shipments, with recovery expected by early 2028.

Global smartphone SoC shipments declined 8% YoY in Q1 2026, according to Counterpoint Research’s latest Global Smartphone SoC Shipments Preliminary View report. The ongoing memory crunch is impacting both smartphone OEMs and SoC vendors’ new product development while forcing them to optimize their product portfolios. The premium segment has remained relatively resilient, with higher costs largely passed on to end consumers. Meanwhile, the entry-level OEMs are increasingly adopting lower-cost chipsets to keep smartphone prices competitive.

Qualcomm and MediaTek recorded double-digit declines in shipments. In contrast, Apple, Samsung, Google and UNISOC posted positive growth. Their integrated supply chains helped Apple, Samsung and Google to better mitigate the impact of the ongoing memory crunch.

Commenting on the smartphone SoC vendor dynamics, Senior Analyst Shivani Parashar said, “Qualcomm and MediaTek were the most affected by the ongoing memory shortage, though for different reasons. Qualcomm was expected to benefit from premiumization, but the impact was limited due to Samsung’s Galaxy S26 series using both Snapdragon 8 Elite Gen 5 and Exynos 2600, along with softer demand for the Xiaomi 17 series. MediaTek, on the other hand, faced greater pressure in the entry-level segment. We expect many OEMs will shift to UNISOC chipsets to reduce costs. At the same time, weaker growth in the mid- and premium tiers, coupled with the delayed launch of the Dimensity 9500+, further weighed on MediaTek’s performance.”

Global Smartphone SoC Shipments Share by Vendor, Q1 2025 vs Q1 2026

Source: Counterpoint Research Global Smartphone SoC Shipments Tracker, Q1 2026

Parashar added, “UNISOC is set to benefit from the low-end 4G segment as well as rising design wins in entry-level 5G smartphones. Support from Chinese brands such as Redmi and Pocophone helped drive its double-digit YoY shipment growth in Q1 2026.”

Memory prices increased 50%-55% QoQ in Q1 2026, and we expect a further rise of 80%-85% QoQ in Q2 2026. The sharp increase in memory costs, combined with the ongoing Middle East conflict, poses risks to smartphone supply chains, logistics, and overall costs.

Commenting on smartphone SoC market outlook, Principal Analyst Soumen Mandal said, “We expect smartphone SoC shipments to decline by double digits in Q2, with the situation likely to worsen in the second half of the year. The memory shortage is expected to continue until the second half of 2027. Both smartphone OEMs and chipset vendors are delaying product launches, holding back new versions and adjusting their spending on new product development to navigate the challenges.”

Mandal added, “Smartphone SoCs for the entry and mid-price segments will see a decline due to the impact of memory crisis, while the premium smartphone SoC segment will see a decline in shipments due to delays in SoC launches from MediaTek and Qualcomm in Q2 2026.”

The supply chain is not expected to return to normal until at least early 2028. Smartphone SoC shipments will likely see a double-digit YoY decline in 2026.

{kind=link}