Prostock-Studio/iStock via Getty Images

As companies grow larger, they become far more complicated. It becomes increasingly important for management and shareholders to have some idea of whether or not the company is operating optimally. This is especially true when it comes to the countless sizable transactions that the companies in question must ultimately engage in for the purpose of their day-to-day operations. One company that’s dedicated to meeting this need is Coupa Software (NASDAQ:COUP). Although shares of the company are not exactly cheap, they don’t look overly priced for an enterprise that’s growing as quickly as it is. The stock is also trading near the low end of the scale compared to similar businesses. But of course, especially during turbulent times, this picture could change on a dime. And what better time to re-evaluate the status and health of a company like this than when management reports financial results for the most recent quarter. Luckily, such a day is just around the corner, with the company due to report financial performance covering the second quarter of its 2023 fiscal year after the market closes on September 6th.

Understanding business spend management

According to the management team at Coupa Software, the company’s operations center around a concept known as business spend management. As this concept’s name suggests, the picture is as simple as keeping track of and managing how companies spend their money. The company provides this service through its own cloud-based platform that has connected its existing customers with more than 7 million suppliers across the planet. Through these connections, the company provides greater visibility into and control over how companies spend their money. But it also helps them to optimize their supply chains and to manage their own liquidity.

Author – SEC EDGAR Data

The company prides itself in having a simple-to-use platform that is incredibly flexible, even being mobile-friendly. And using the data, the company is able to provide valuable insights regarding the spending activities of the firms on its platform so that customers can use that data to gain greater control over their various spending-related activities. At the heart of the company’s platform lies its ability to provide customers with procurement, invoicing, expense management, and payment solutions, but the company also has expanded into other initiatives. For instance, its Coupa Community.ai capabilities that are based on the data it collects, help customers by offering up prescriptive spending insights and risk management recommendations.

Author – SEC EDGAR Data

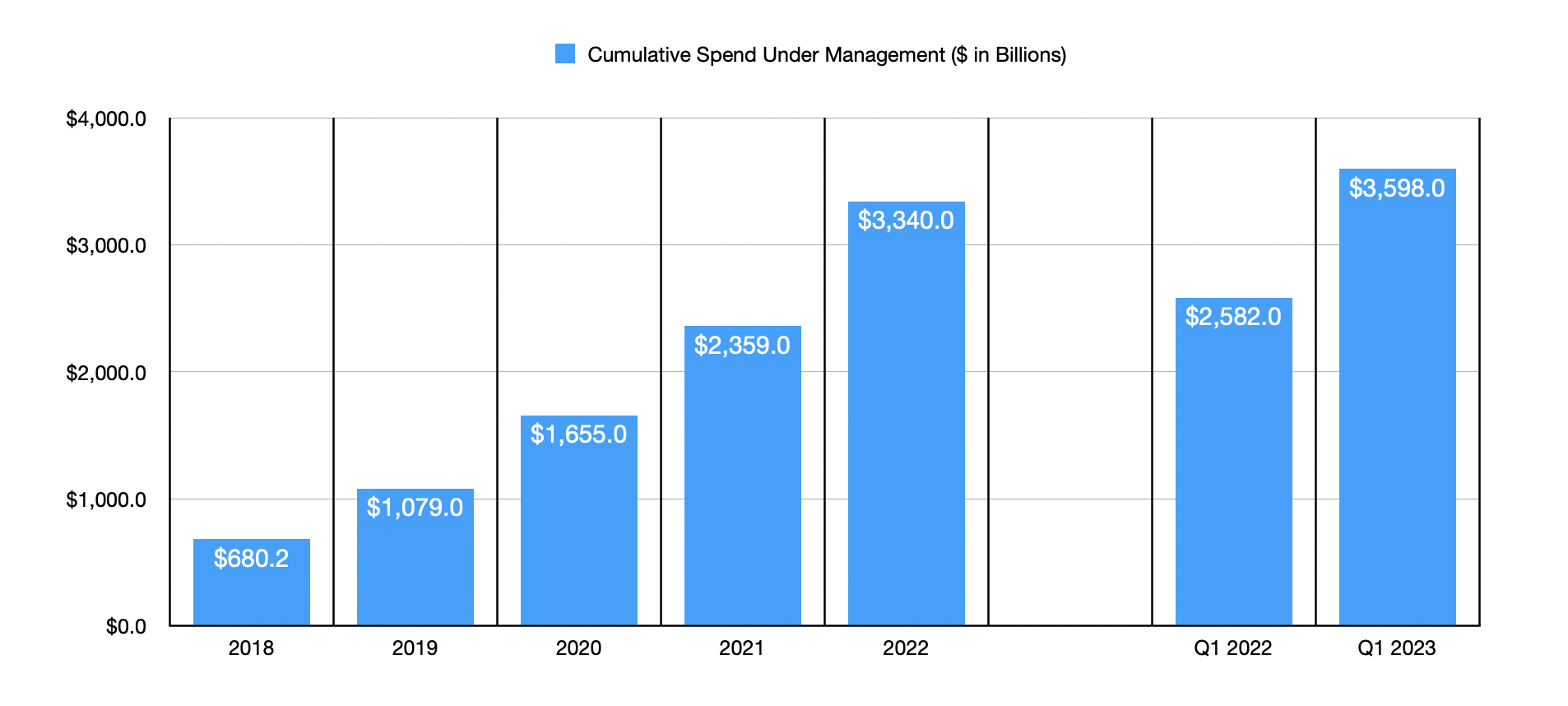

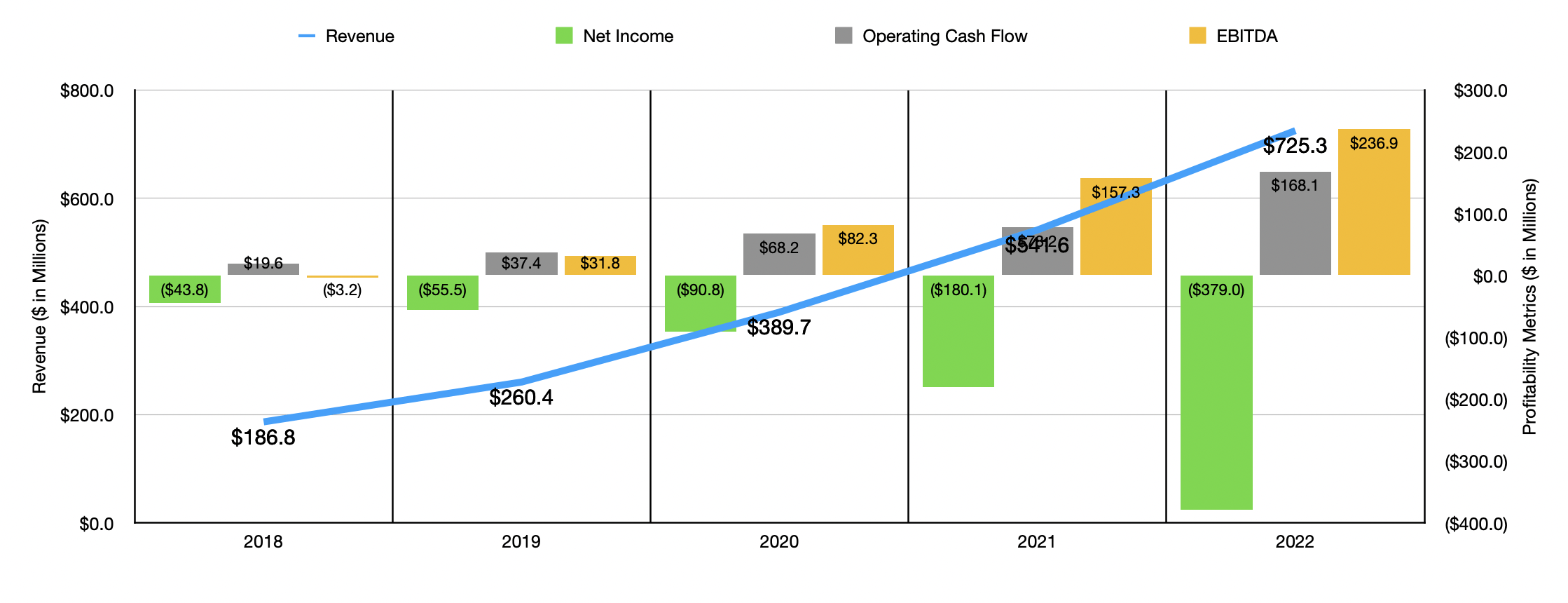

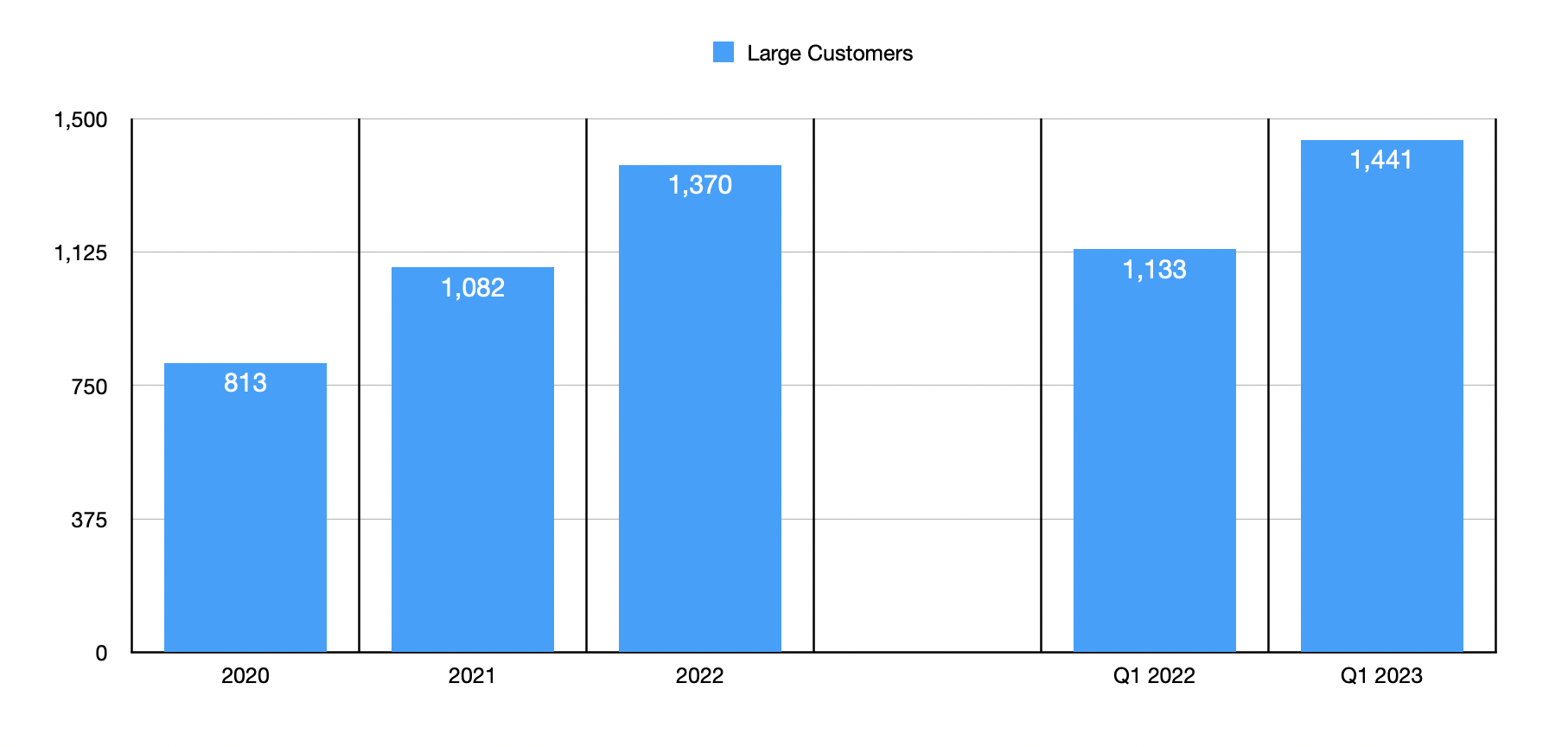

Over the years, the management team at Coupa Software has done a really good job growing the company’s top line. Revenue expanded in each of the past five years, climbing from $186.8 million in 2018 to $725.3 million in fiscal year 2022. One of the key drivers of this increase was a significant rise in the cumulative spending tracked by the company’s platform. As its customer base increased, the company saw this spending rise from $680.2 billion to $3.34 trillion. Between 2019 and 2022, remaining performance obligations, which are commonly referred to as backlog, rose from $498.6 million to $1.28 billion. And between 2020 and 2022, the number of customers that the company bills at an annual amount of $100,000 or more rose from 813 to 1,370.

Author – SEC EDGAR Data

On the bottom line, things have been a bit more volatile. Any fast-growing company is bound to generate some losses. And that is precisely what we have seen in recent years. In fact, between 2018 in 2022, the company’s bottom line has worsened, with net losses going from $43.8 million to $379 million. Although this has been the case, operating cash flow has improved, rising from $19.6 million to $168.1 million over the same window of time. Meanwhile, EBITDA for the company also improved, going from negative $3.2 million to positive $236.9 million over the past five years.

Author – SEC EDGAR Data

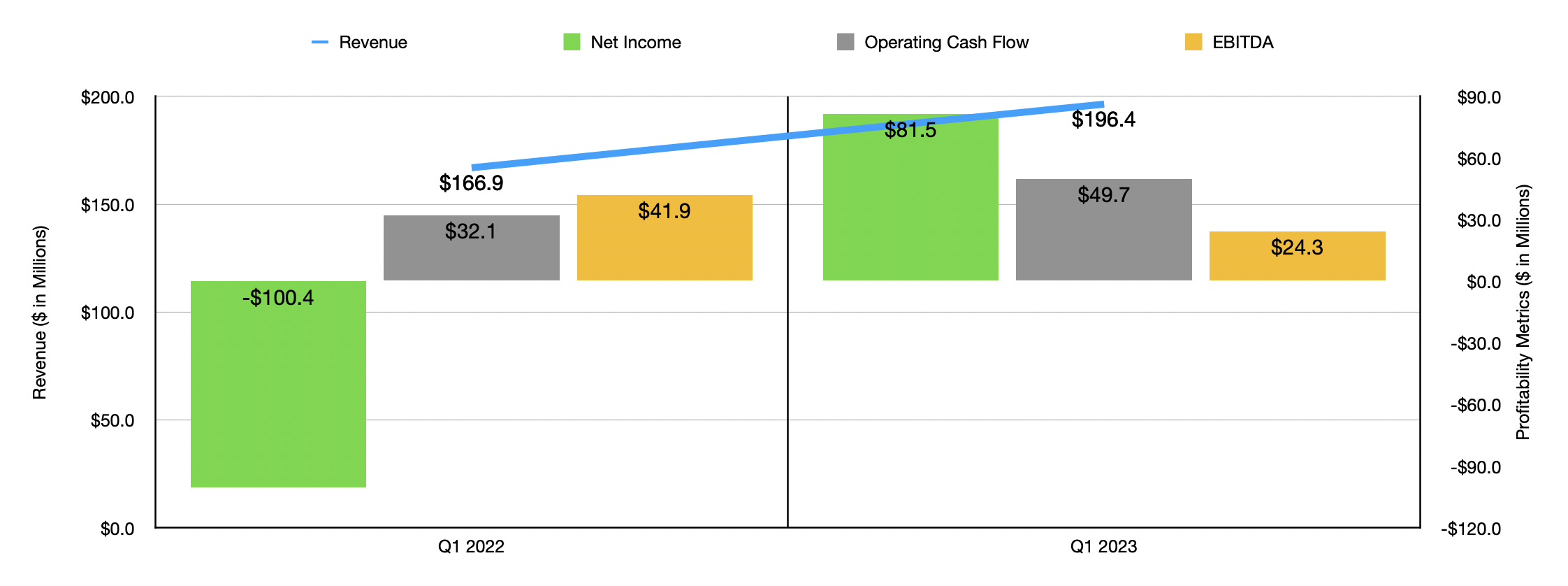

The company’s performance has continued to come in strong, in most respects, during the 2023 fiscal year. For the first quarter of the year, sales came in at $196.4 million. This compares favorably to the $166.9 million generated one year earlier. This rise can be attributed in large part to an increase in large customers from 1,133 to 1,441. These customers, in turn, pushed keep me out of spending from $2.58 trillion to $3.60 trillion. And remaining performance obligations for the company grew from $972.9 million to $1.32 billion. When it comes to profitability, the picture has been somewhat mixed. The firm went from generating a net loss of $100.4 million in the first quarter of 2022 to a loss of $81.5 million the same time this year. Operating cash flow also improved, climbing from $32.1 million to $49.7 million. But EBITDA for the company worsened, dropping from $41.9 million to $24.3 million over the same timeframe.

Author – SEC EDGAR Data

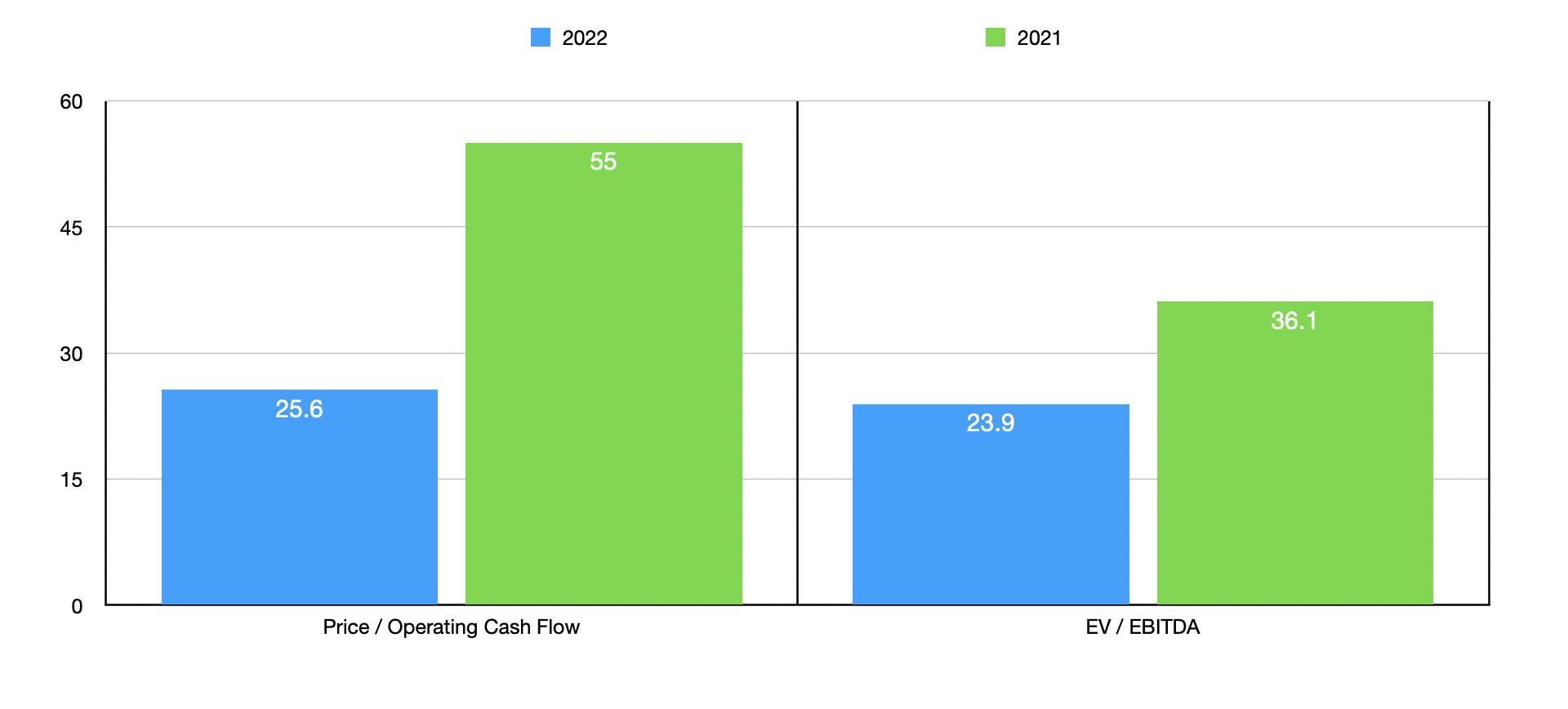

In terms of valuing the company, it’s worth noting that management is forecasting revenue this year of between $838 million and $843 million. At the midpoint, this would translate to a year-over-year increase of 15.9%. Adjusted earnings per share, meanwhile, should come in at between $0.21 and $0.27. In absolute dollar terms, this would translate to adjusted profits of $21.2 million. We don’t have any estimate as to what official earnings would be. And, in general, earnings are a bit problematic from a valuation perspective. So instead, I decided to value the company based on results achieved in the 2022 fiscal year. Following this approach, the company is trading at a forward price to operating cash flow multiple of 25.6 and at an EV to EBITDA multiple of 23.9. As the chart above illustrates, these prices are considerably lower than if we used the results from the 2021 fiscal year. As part of my analysis, I also compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 4.7 to a high of 63.4. Two of the five companies were cheaper than Coupa Software. And when it comes to the EV to EBITDA approach, the range was from 8.9 to 65.7, with only one of the companies cheaper than our prospect.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Coupa Software Incorporated | 25.6 | 23.9 |

| DoubleVerify Holdings (DV) | 63.4 | 52.7 |

| SPS Commerce (SPSC) | 44.5 | 46.1 |

| NCR Corporation (NCR) | 4.7 | 8.9 |

| Tenable Holdings (TENB) | 39.8 | 64.2 |

| Box Inc. (BOX) | 15.8 | 65.7 |

Given current economic conditions, it’s not unthinkable that the financial performance of Coupa Software could change materially from quarter to quarter. Because of this, investors should keep a close eye on results reported for the second quarter when management reports them on September 6th. At present, analysts are anticipating revenue of nearly $204 million. That would represent an increase of 13.8% over the $179.2 million reported just one year earlier. The loss per share of the company, meanwhile, should be $1.20, while the adjusted earnings should be $0.09 per share. Using results from the second quarter of last year, the company reported a net loss per share of $1.24 and an adjusted profit per share of $0.26. So the current expectations don’t seem to be terribly far off from what the results were last year.

Takeaway

Based on the data provided, I believe that the future for Coupa Software is definitely bright. Absent something unexpected occurring, the company should continue to grow over the long run. Heading into earnings, investors should keep a close eye on revenue and profitability. But they should also pay attention to cash flow and cumulative spending data on the company’s platform. These figures, combined with large customer subscription data and remaining performance obligations, will go a long way toward determining what the near-term prospects of the company will look like. And given how shares are priced both on an absolute basis and relative to similar players as we near the earnings release for the enterprise, I would say that it makes for a reasonable, if pricey, ‘buy’ prospect.