- China, the world’s fastest-growing connected car market, captured 37% of global connected car sales in Q3 2025 on 7% YoY growth, driven by local automakers.

- Driven by fast software innovation, aggressive 5G rollouts and competitive pricing, Chinese automakers’ connected car sales grew 17% YoY in Q3 2025, increasing their share in China’s connected car market to 68% compared to 63% in Q3 2024.

- Deep partnerships with local tech giants let Chinese automakers ship richer digital experiences faster and at lower cost than global rivals.

China strengthened its position as the world’s largest connected car market in Q3 2025, with its sales growing 7% YoY to expand the country’s share of the global connected car market to 37%, according to Counterpoint’s Global Connected Car Market Tracker, Q3 2025. “This reflects not only China’s scale as the world’s largest automotive market, but also the rapid democratization of connectivity across all vehicle segments and price bands,” said Associate Director Kevin Li.

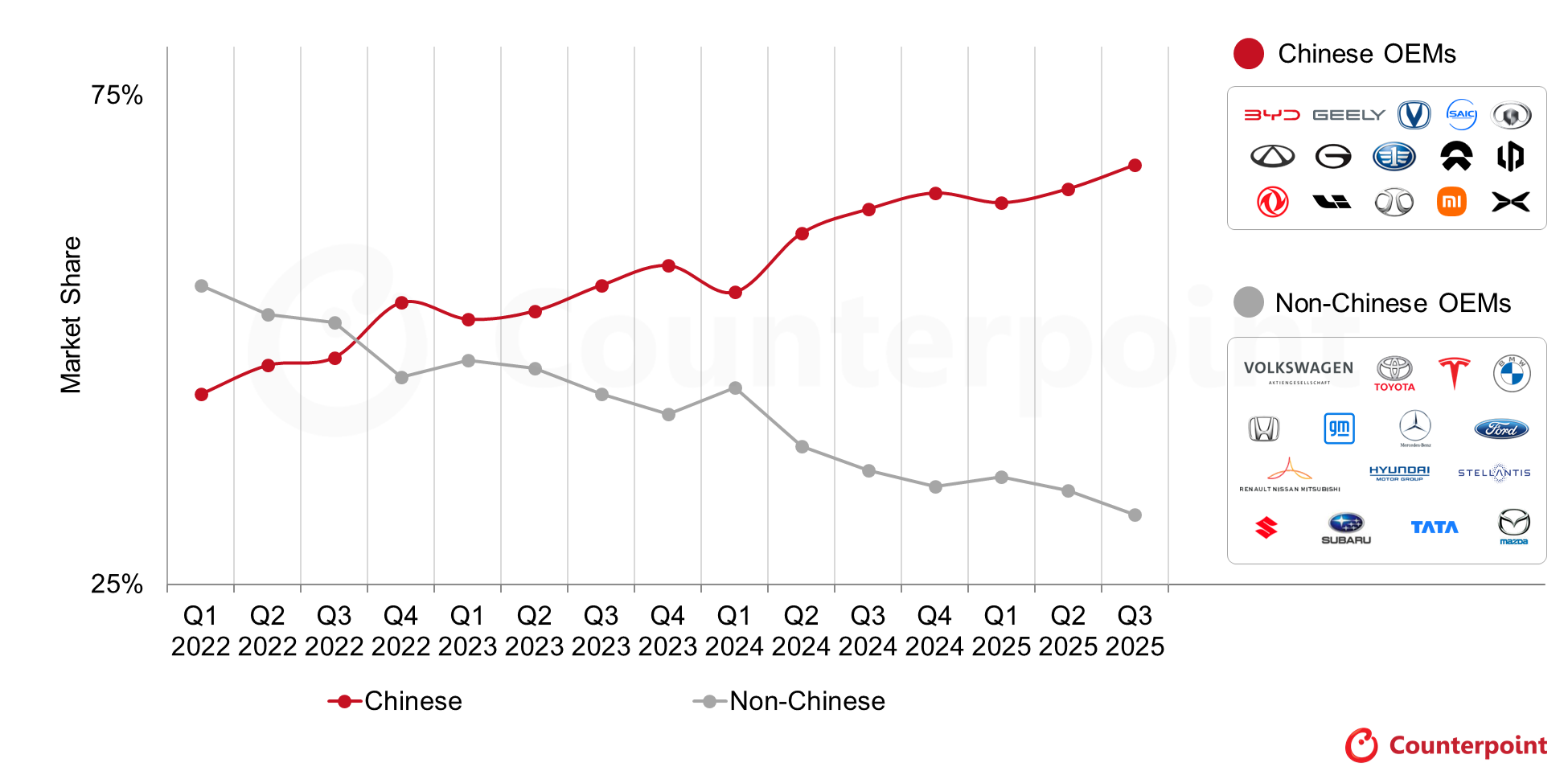

China Connected Car Sales Share by OEM Country of Origin

Source: Counterpoint’s Global Connected Car Tracker, Q3 2025

In the last three years, Chinese automotive groups have undergone a stunning market share realignment. Their share of China’s connected car market grew from roughly 48% in Q3 2022 to 68% in Q3 2025, thanks to their view of connectivity as a key technology that enables them to better compete in the world’s largest automotive market while increasing their share in the global market, driven by higher connectivity penetration compared to non-Chinese automakers. According to Counterpoint data, non-Chinese automakers’ connected car sales share in China sharply contracted from 52% in Q3 2022 to 32% in Q3 2025.

Chinese players’ connected car sales grew 17% YoY in Q3 2025. This has not been a gradual shift in margin, but a structural realignment. Chinese automakers have made connectivity a standard offering across their entire lineups, including entry-level and mid-market models. On the other hand, non-Chinese groups have focused on providing connected features in premium segments, leaving mass-market vehicles largely undifferentiated.

Chinese automakers have forged deep partnerships with local technology providers, including Baidu and AutoNavi for mapping, Huawei for domain controllers, Alibaba for cloud services and payments, and Tencent for in-car entertainment. “These partnerships accelerated development cycles and reduced costs, enabling affordable deployment of rich digital experiences across price tiers,” said Associate Director Greg Basich.

Expanding 5G coverage, faster OTA (over the air) update cycles, and intense competition among tech-focused automakers are further pushing connected features deeper into mid-range and entry-level models. Connectivity is no longer an ancillary service in China; it is the primary architecture of automotive competition. Chinese groups understood this transition before foreign competitors and executed decisively.