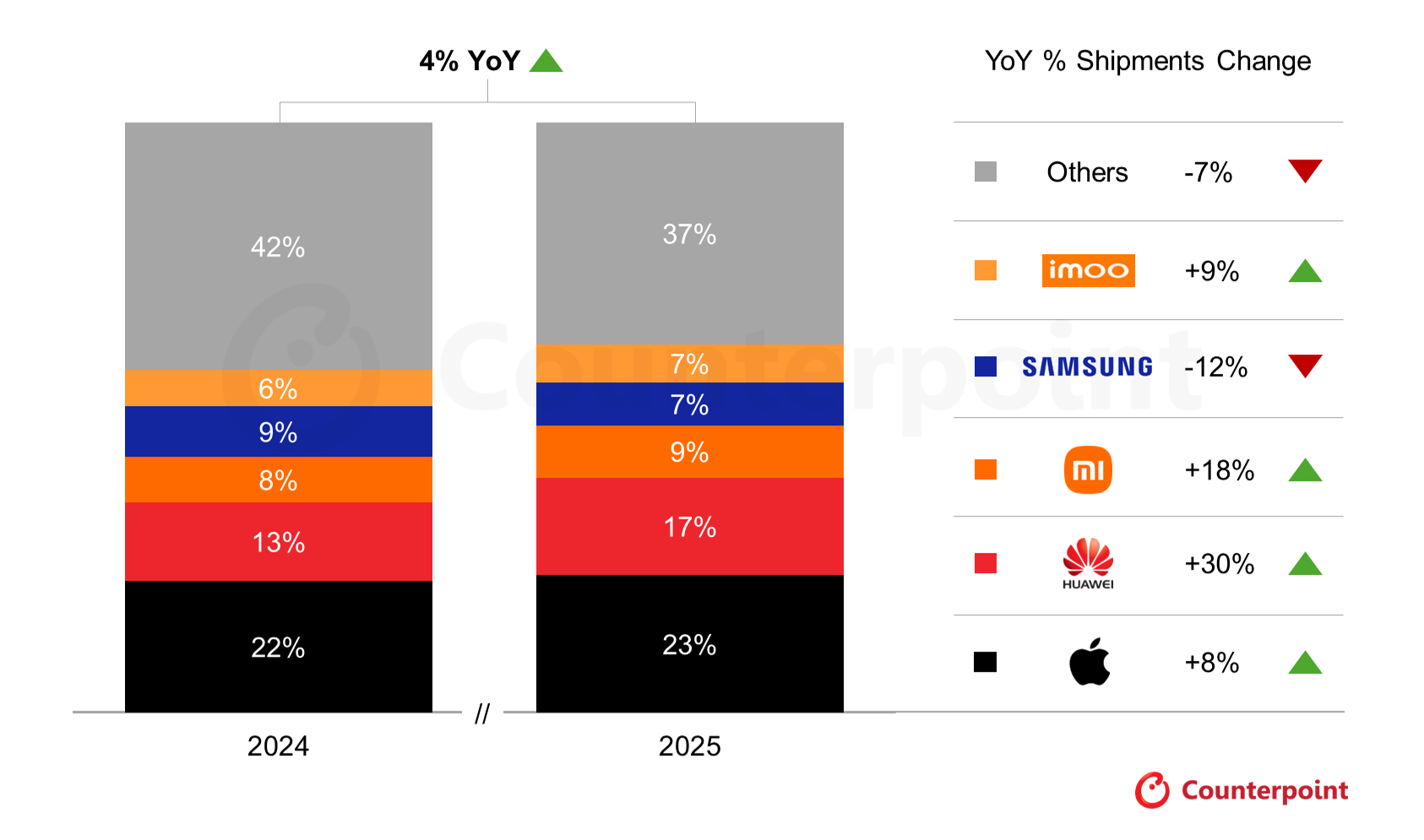

- Global smartwatch shipments grew 4% YoY in 2025, following a decline in 2024, with Apple and Huawei driving overall momentum.

- China emerged as the fastest growing market, supported by strong performances from domestic brands such as Huawei, Xiaomi and Imoo.

- Apple posted its first YoY shipment growth since 2022, fueled by a comprehensive portfolio refresh across its smartwatch lineup.

- Cellular smartwatch shipments grew 6% YoY, driving the connected ecosystem.

Global smartwatch shipments grew 4% YoY in 2025, recovering from a decline in 2024, according to Counterpoint Research’s Global Smartwatch Shipments Tracker, Q4 2025. The market’s recovery was driven by a shift in the competitive landscape, marked by hardware and software upgrades from key market players, consumers’ preference for more technologically advanced smartwatches, and an industry-wide focus on health functionalities. China led the global rebound with strong demand for leading domestic brands including Huawei, Xiaomi, and Imoo. Huawei recorded the highest shipment growth among the top five brands as it saw strong consumer uptake for its advanced, competitively priced products in China. The brand also benefitted from the government subsidies supporting electronics sales in the country.

Commenting on the market recovery, Senior Research Analyst Anshika Jain said, “Apple witnessed its first YoY shipment growth since 2022. This growth was driven by a complete refresh of its portfolio with the introduction of the Series 11, Ultra 3, and SE 3. With these launches, Apple offered products that catered to a wide consumer base, ranging from the more affordable Watch SE 3 to the ultra‑premium Watch Ultra 3. Additionally, the portfolio received significant technological upgrades, including the series‑wide introduction of 5G Redcap support, hypertension notification, and satellite connectivity in the Watch Ultra 3. As a result, consumers who had been delaying their purchases in anticipation of a substantially improved smartwatch finally had compelling options available.”

Global Smartwatch Shipments Market Share, 2024 vs 2025

Source: Counterpoint Research

Emphasizing on the global market, Jain added, “The smartwatch market continued its premiumization trajectory in 2025, with average selling price (ASP) rising 5% YoY. Due to growing health and fitness awareness, consumers have been moving up the pricing ladder and choosing more accurate, feature‑rich devices. Smartwatches priced below $200 saw a 9% YoY decline in shipments, whereas the $200-$400 segment recorded a substantial 48% YoY increase. Even basic smartwatches saw a 34% ASP uplift as brands integrated AI and advanced sensors, pushing entry‑level pricing higher.”

Commenting on the cellular connectivity penetration, Associate Director David Naranjo said, “Shipments of smartwatches supporting cellular connectivity increased by 6% YoY. Growth in cellular-enabled models was supported by advanced health monitoring and emergency SOS capabilities, making them more attractive to mainstream users. Apple drove this momentum with its refreshed lineup, including the Watch Series 10. Xiaomi also strengthened its cellular portfolio with the Redmi Watch 5 LTE and Redmi Kids Watch. Apple’s introduction of 5G support in its Watch Series 11 is expected to accelerate industry-wide adoption of 5G connectivity. In 2025, connectivity is no longer limited to cellular technology alone. Google, Garmin, and Apple also introduced satellite connectivity, highlighting the industry’s focus on developing smartwatches that function as standalone devices.”

Smartwatches are transforming from being mere accessories to standalone devices that support connectivity and comprehensive health and fitness monitoring. Brands are now expanding their capabilities to track a wider range of health conditions, from atrial fibrillation, blood pressure, and sleep apnea to developing technologies aimed at monitoring blood glucose levels. With ongoing advancements and rising consumer interest in next‑generation smartwatches, smartwatch shipments are expected to record high-single‑digit percentage YoY growth in 2026.

{kind=link}