AndreyPopov

Introduction

Artificial Intelligence (“AI”) is everywhere. Everyone is talking about it.

That’s no surprise, as it is both cool and scary. Just yesterday, I asked Google Gemini to give me a full overview of the world’s best olive oils and the reasons why they are so good.

Within seconds, I got a report that would have taken me at least 45 minutes to write without AI support.

This is obviously just one example of the power of AI – and it’s not even a good one, I have to admit, as AI is capable of way more than telling me which overpriced bottle of olive oil to buy next.

AI can generate code, plan entire trips, generate pictures and videos, produce real-life-like (Instagram) influencers, produce music, and so much more.

Just writing this makes me feel like I’ll be out of a job soon.

Unfortunately, the Wall Street Journal agrees with me, as it published this headline last month:

Wall Street Journal

According to the report, two-thirds of white-collar workers improve their productivity using AI.

That said, the report also mentioned that AI is getting so good that a lot of management jobs are redundant, causing companies to cut jobs that won’t return even if business demand picks up.

United Parcel Service said that it would cut 12,000 jobs-primarily those of management staff and some contract workers-and that those positions weren’t likely to return even when the package-shipping business picks up again. The company has ramped up its use of machine learning in processes such as determining what to charge customers for shipments. As a result, the company’s pricing department has needed fewer people.

I’m not bringing this up to scare anyone but to make the point that none of this is possible without the underlying hardware. That’s where data centers come into play.

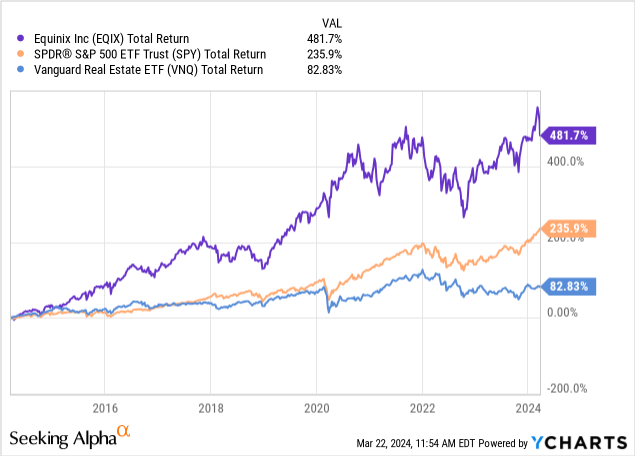

The biggest data center company in the world is Equinix (NASDAQ:EQIX). With a market cap of more than $75 billion, it’s also one of the biggest REITs in the world – across all sectors.

Over the past ten years, the REIT has returned more than 480%, beating the S&P 500 by a huge margin. It has beaten the subdued 82% return of the Vanguard Real Estate ETF (VNQ) by an even bigger margin.

My most recent (co-produced) article on the stock was written on October 31, shortly after the company hiked its dividend by 25%.

Since then, shares have returned 12% despite a drop due to a negative research report.

In the remainder of this article, I’ll give you my take on this data center giant.

So, let’s get to it!

Secular Growth & Elevated Returns

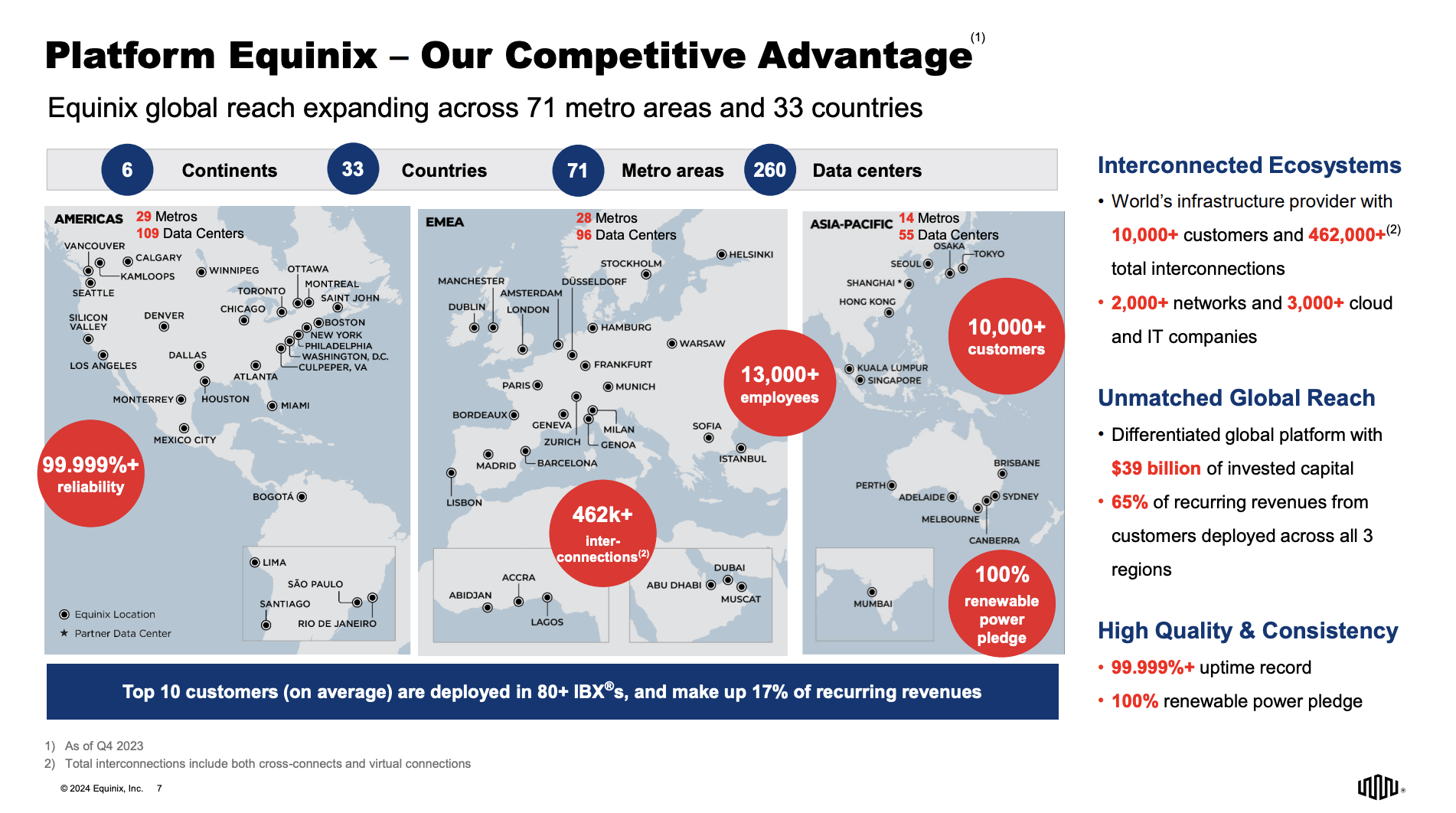

Equinix is a giant. Behind its $75 billion market cap is a business that consists of 260 data centers in 33 countries with a 99.999% uptime record that serves more than 10,000 customers.

Equinix

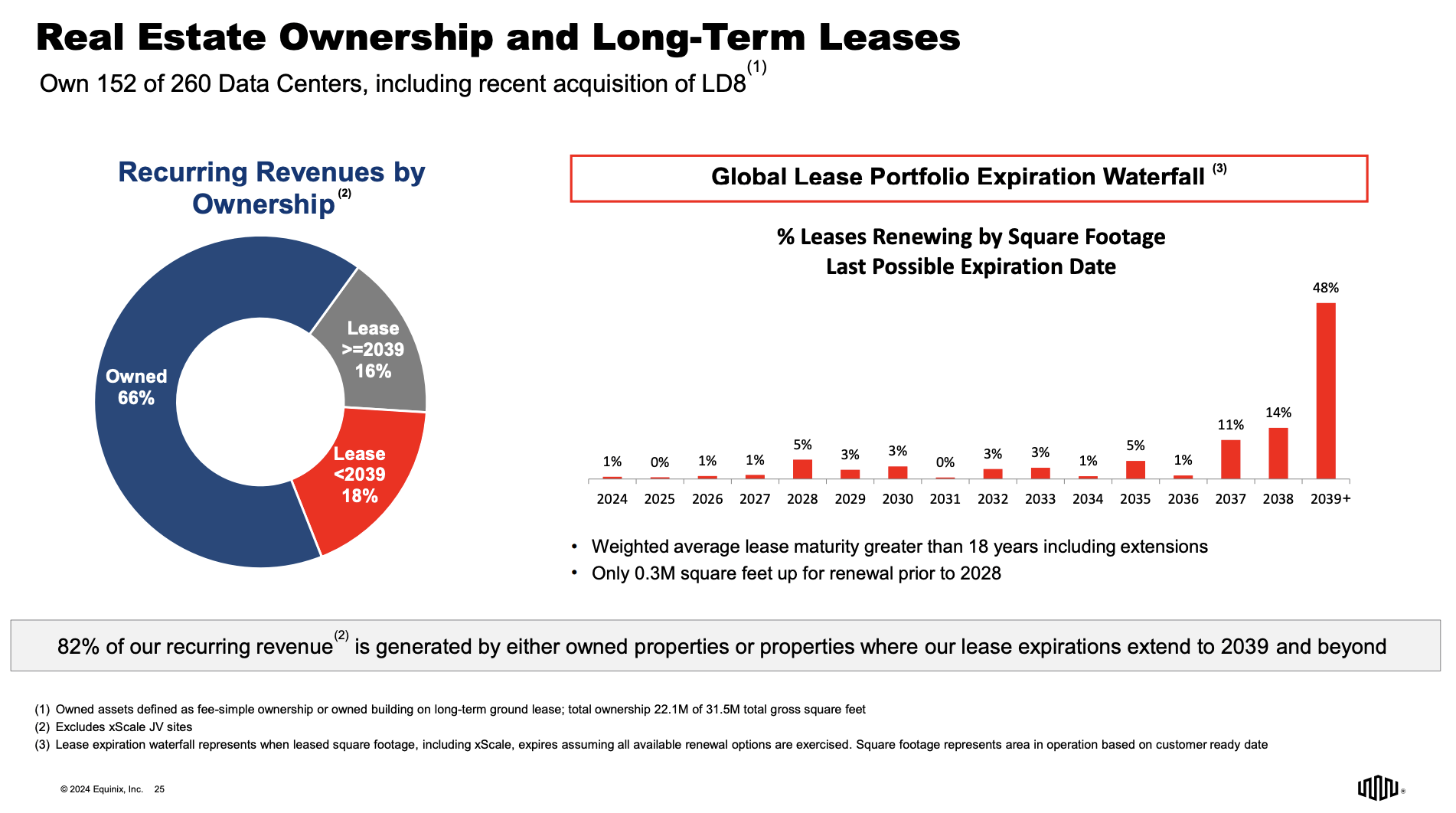

As we can see below, 82% of the company’s recurring revenue is generated either by owned properties or properties where lease expirations extend to 2039 or beyond.

It owns 152 of its 260 data centers.

Equinix

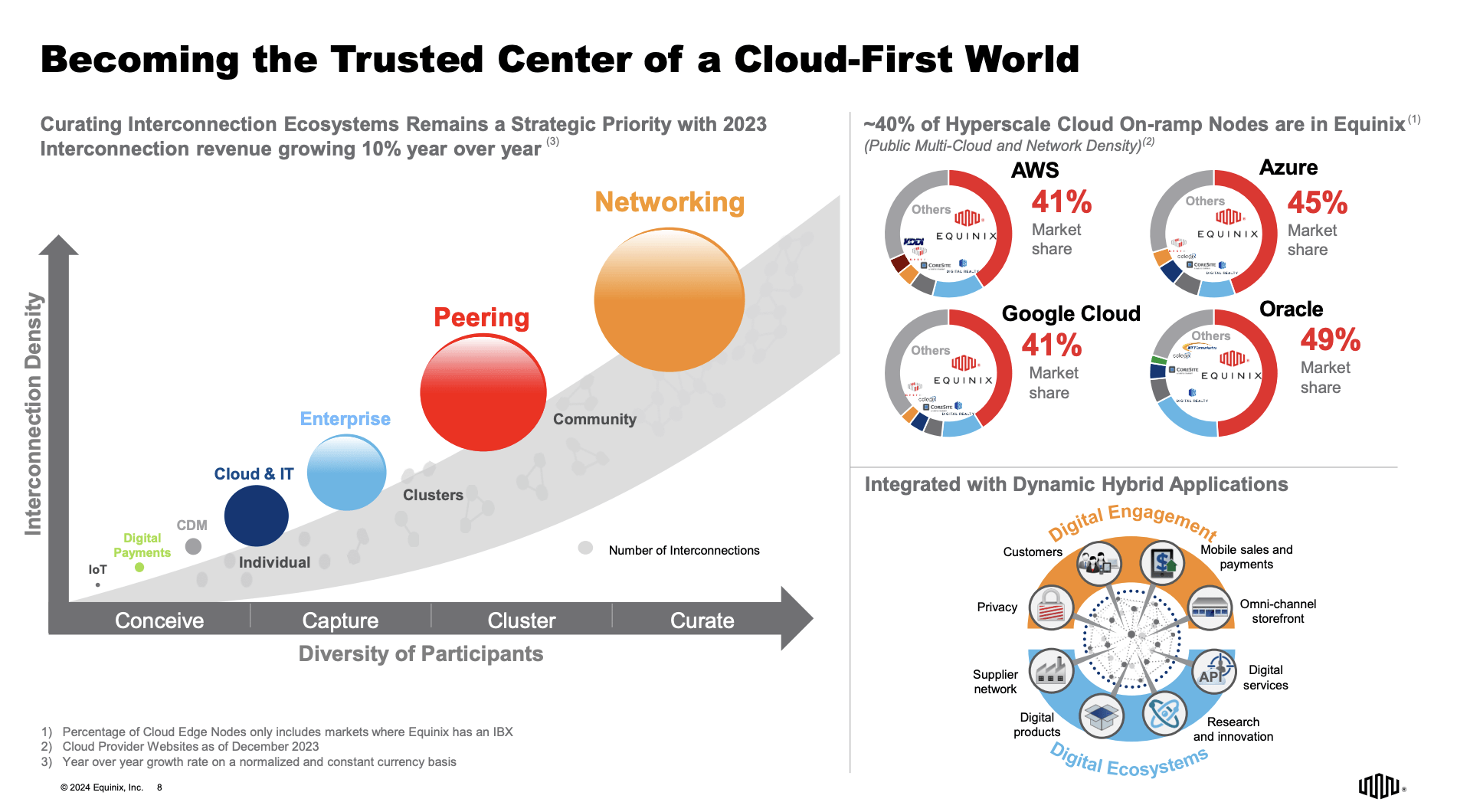

The company is the go-to destination for “hyper-scalers,” including Amazon Web Services, Azure, Google Cloud, and Oracle.

In each of these services, it has a market share of more than 40%, with its number two competitor being far behind.

Equinix

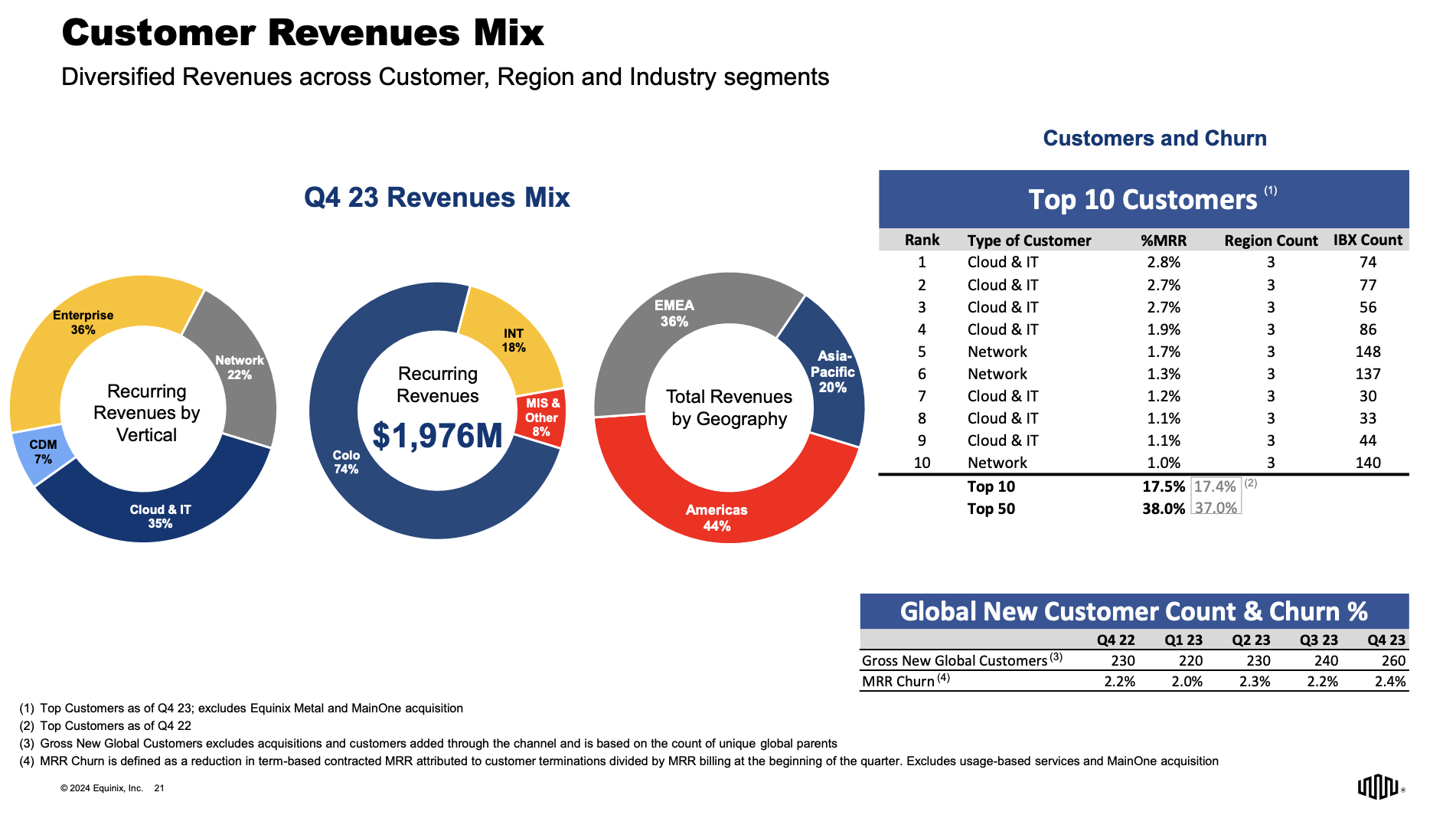

What sets the company apart is that it is available everywhere. As we just saw, it has a massive footprint that has benefits for global players.

In fact, the company’s non-U.S. business accounts for almost 60% of its revenues.

Equinix

While the company saw some higher churn in its fourth quarter (2.4% versus 2.2% in 3Q23 – as seen in the overview above), management remains extremely upbeat about demand and utilization rates, especially in light of its xScale bookings. xScale assets are hyperscale partnership data centers.

Here’s what the company said during this month’s Morgan Stanley Technology, Media & Telecom Conference when it was asked about demand developments (emphasis added):

Simon Flannery

Great. Well, maybe we just pick into the guide a little bit. You had record xScale bookings, 90 megawatts, I think. And that spoke to some of the AI demand. But then you still have that elevated churn. So is it very, very different between hyperscale demand and enterprise demand or…

Keith Taylor

Probably a little bit like the equity markets, right, Magnificent 7 to some degree. Look, the skill demand is very real. And as we said, we sold about 90 megawatts, $1.9 billion of — $1.8 billion of contract value, 15-year term. The hyperscalers that you know, that you would expect are consuming that. We’re about close to 85% utilized of what we’ve announced and what we’ve built. If you add to that what we’re negotiating right now, we’re probably north of 95% sold out. And we have a commitment to put up roughly 800 megawatts, and we’re at 330 right now. And so we have a runway — a nice runway ahead of us.

In other words, like the equity market, the Mag 7 stocks/companies are running the show.

The good news is that the company sees strong demand, is not overbuilding, and expects consistent room for expansions.

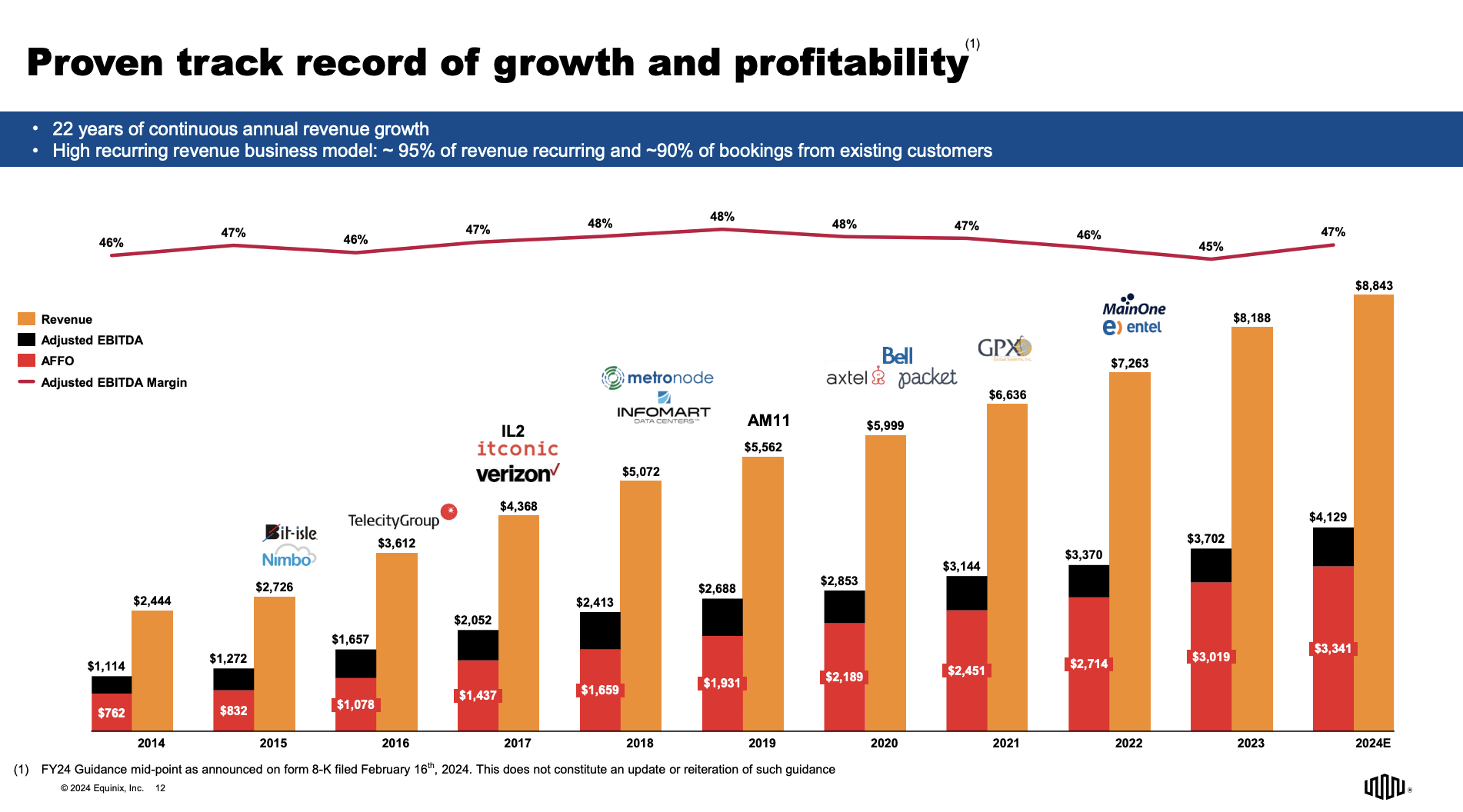

In fact, this year, the company is expected to generate $8.8 billion in revenue and $3.3 billion in adjusted funds from operations – that’s 7.3% and 10.0% higher compared to last year, respectively.

In 2014, the company generated just $2.4 billion in revenues.

Even better, the company is expected to maintain consistent adjusted EBITDA margins in the high-40% range. That’s a good sign in times of elevated inflation.

Equinix

With that said, the company also has a dividend.

Currently, Equinix pays $4.26 per share per quarter. This translates to a yield of 2.1%.

That may not seem like a lot.

However:

- The five-year dividend CAGR is 10.5%. The most recent hike was 25%.

- This year, the company is expected to generate $34.99 in AFFO. This implies a payout ratio of just 49%.

- Growth expectations are elevated, hinting at consistent dividend growth in the future:

| Year | AFFO Growth |

| 2024E | 9% |

| 2025E | 8% |

| 2026E | 7% |

These numbers also bode well for its valuation.

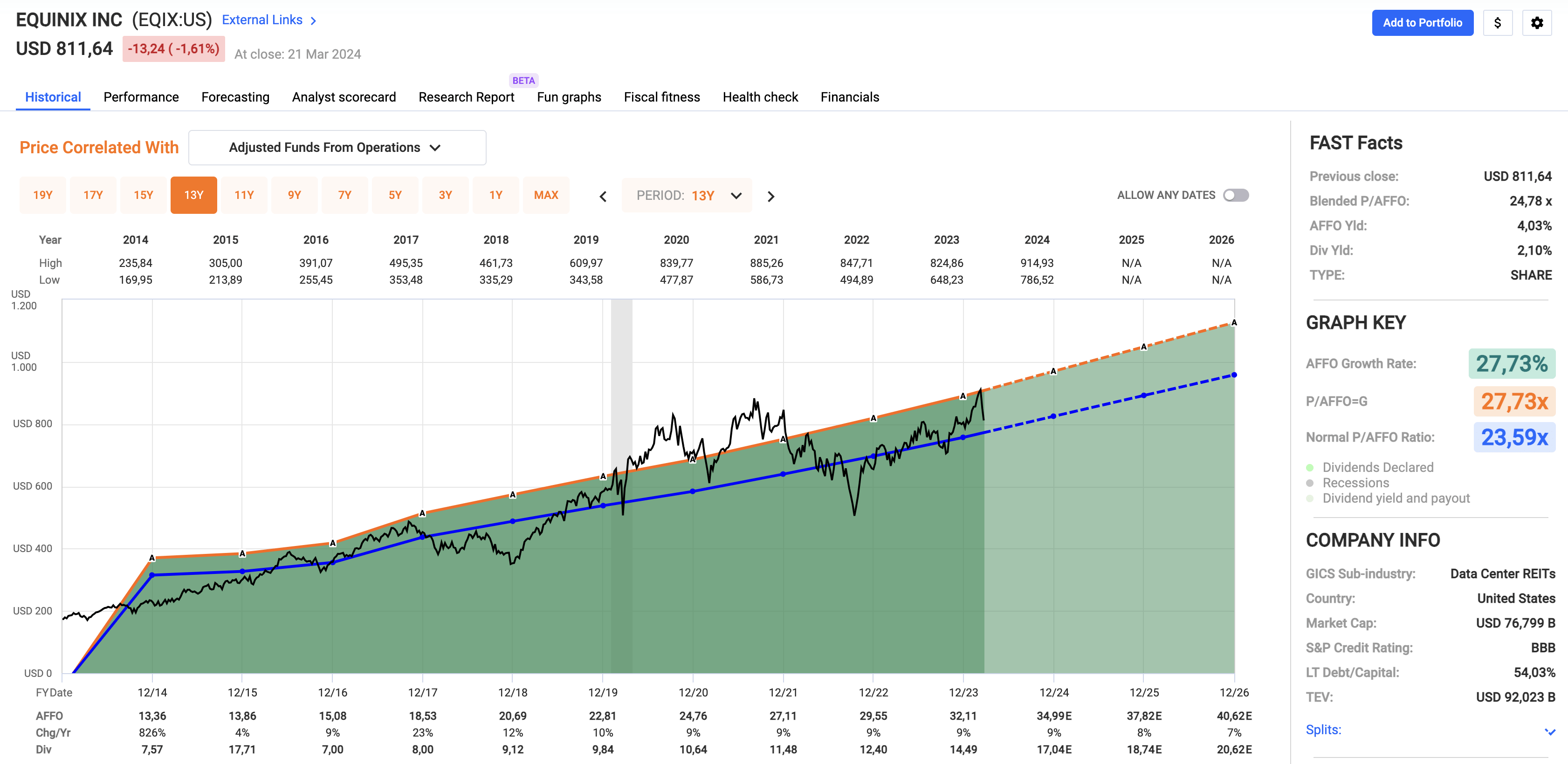

According to the chart below, where I also got the AFFO growth rates I just showed you:

- EQIX has a normalized P/AFFO multiple of 23.6x

- The current blended P/AFFO multiple is 24.8x.

- The combination of expected AFFO growth and a 23.6x multiple gives us a fair price target of roughly $960. That’s roughly 20% above the current price.

FAST Graphs

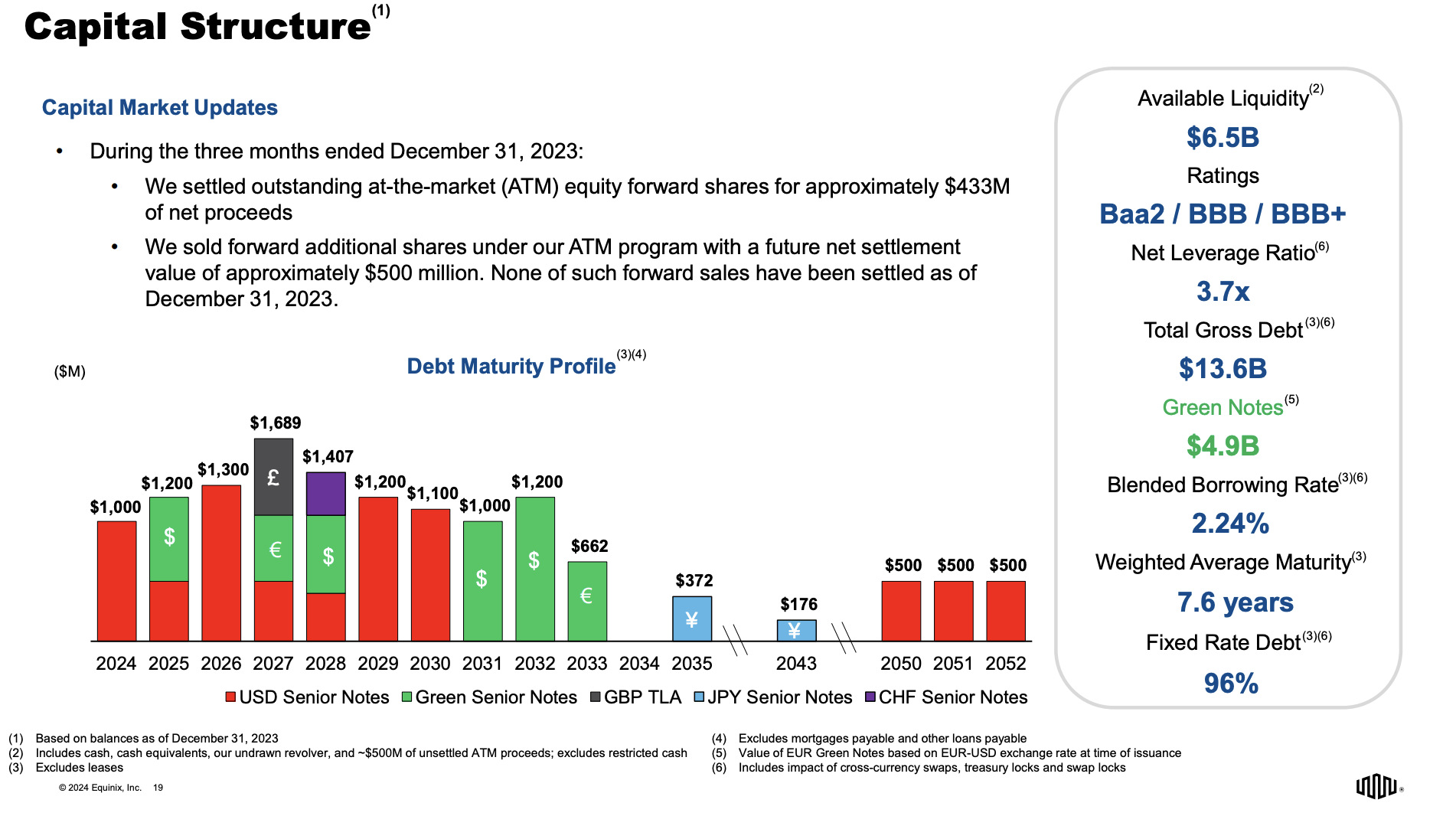

The company also comes with a fantastic balance sheet. It has an investment-grade BBB+ rating, 96% fixed-rate debt, $6.5 billion in liquidity, a net leverage ratio of less than 4x EBITDA, and a well-laddered maturity profile.

Equinix

With that said, I would usually end the article here.

However, there’s a big elephant in the room.

The Hindenburg Sell-Off

Usually, when others publish something I disagree with, I ignore it. After all, my goal isn’t to disagree with others but to present my view on things.

However, in this case, we need to address what Hindenburg Research just said about Equinix, as it caused the stock to drop significantly.

Even worse, it is making some harsh accusations, including that the company apparently manipulates its financials to make growth look better and allow management to receive bigger bonuses.

Here’s the full research in case you’re interested: Hindenburg Research On EQIX.

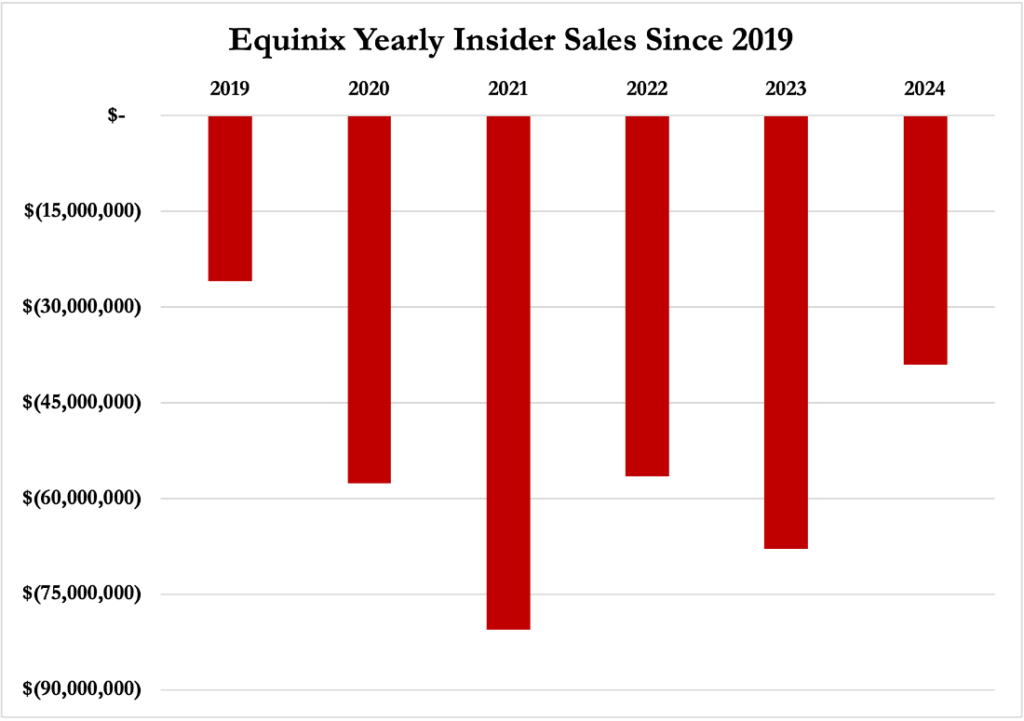

Although I agree with Hindenburg that it is not a good sign that insiders are aggressively selling stock (see the chart below), I disagree with a number of other things.

Hindenburg Research

For example, the company makes the case that EQIX is more expensive than its peers.

While it is certainly the most expensive among its peers, Hindenburg included companies like American Tower (AMT), which is mainly cell tower-focused. Moreover, EQIX has been a better performer than Digital Realty (DLR) and Iron Mountain (IRM), which justifies a higher multiple.

Hindenburg Research

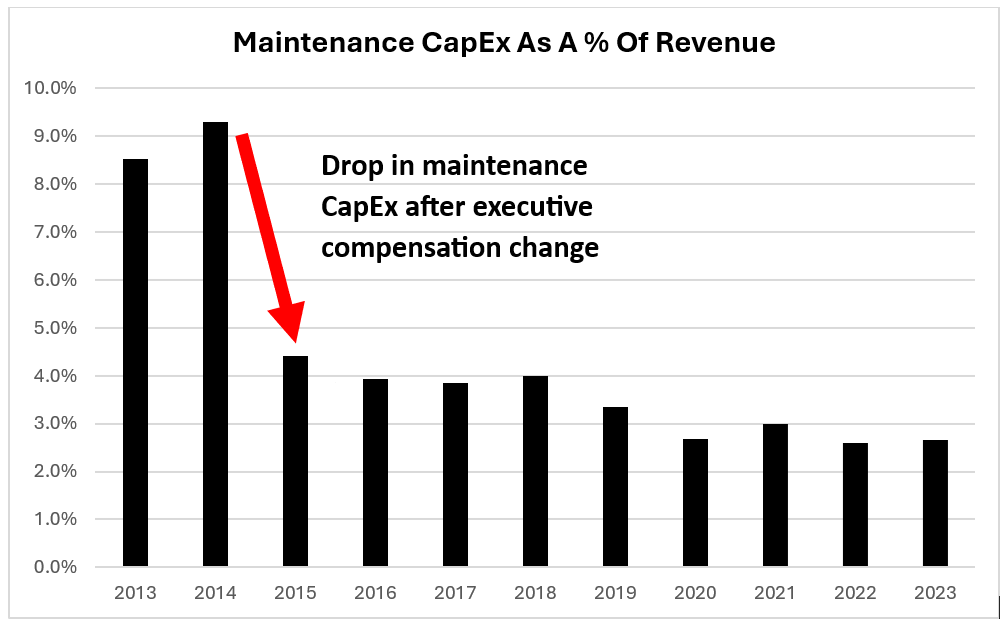

Moreover, the company makes the case that IQIX is manipulating its financial numbers by reducing maintenance capital expenditures.

In 2015, The Company Transitioned to REIT Status And Began Using AFFO As A Metric In Determining Executive Bonuses

That Same Year, Equinix Reported A 47% Drop In Maintenance CapEx, Leading To An Estimated 19% Boost To AFFO

Hindenburg Research

While Hindenburg presents examples of potential maintenance neglect, I believe that the biggest reason for subdued CapEx/revenue is caused by outperforming revenue. It is very hard to prove financial manipulation, and I distance myself from these accusations.

Adding to that, after publishing its research, it got headwinds.

According to Reuters:

Brokerage TD Cowen played down the concerns raised by Hindenburg Research.

“The thesis is largely a re-hashing of a short thesis published in 2022 which we disagreed with. The comments on overselling power capacity are incremental, but (it) is a broader industry practice,” the brokerage said, adding that the share weakness was a “buying opportunity”.

Analysts have said the boom in generative AI will spur demand for the company’s data centers and last month, Equinix forecast annual AFFO above estimates.

I do not have a horse in this race. I have no motivation to defend or attack Hindenburg. However, I had to include it, as it made headlines and caused the stock to drop.

Personally, I believe the bull case for Equinix is strong, and I consider it to be a fantastic AI play that comes with a good valuation and consistently rising income.

It also needs to be said that EQIX is down just 9% over the past four weeks. If the market expected hard evidence of “fraud,” it would likely trade much lower.

Takeaway

Artificial Intelligence’s influence is undeniable, as it reshapes the economy in a major way.

Equinix emerges as a major player in this AI-driven world, providing the infrastructure necessary for AI’s expansion.

Despite recent controversies, Equinix stands firm with its strong fundamentals, global presence, and impressive growth prospects.

As AI continues to flourish, Equinix remains poised for sustained growth and income, making it an attractive investment opportunity for income growth-focused investors seeking AI exposure.

Pros & Cons

Pros:

- Secular Growth: Equinix operates in a sector with tremendous AI tailwinds.

- Global Footprint: With a major network across 33 countries, Equinix offers access to key markets, supporting the needs of the world’s biggest tech companies.

- Key Partnerships: The company’s partnerships with major hyper scalers like Amazon Web Services and Google Cloud ensure strong demand.

- Steady Income: Equinix’s consistent revenue growth and rising dividends provide investors with both value and growth.

Cons:

- Controversy and Risk: The recent Hindenburg report cast doubt on the company’s financial integrity.

- Dependency on AI Growth: While AI growth presents opportunities, Equinix’s rosy outlook is closely tied to the continued expansion of AI.

- Competitive Landscape: Intense competition in the data center industry could impact Equinix’s market share and margins.

- Regulatory Risks: Regulatory changes or legal challenges could negatively impact Equinix’s operations and financial performance.