- Global smartphone shipments in 2026 are expected to shrink 2.1% due to rising memory costs.

- We have revised down our 2026 smartphone shipment forecast by 2.6%pts, with Chinese OEMs seeing the biggest downward revisions.

- In terms of price bands, the low-end segment is the most impacted, but the impact is being felt broadly.

- DRAM price surges have already increased low-, mid- and high-end smartphone BoM costs by around 25%, 15% and 10%, respectively. We are expecting further cost impacts in the 10%-15% range through Q2 2026.

- ASPs have been revised up 6.9% YoY (from 3.6% in our September update) as cost pass-through and portfolio rebalancing move wholesale ASPs higher.

Global smartphone shipments are expected to decline 2.1% in 2026 as surging component costs are likely to impact demand, according to Counterpoint Research’s latest Global Smartphone Shipment Tracker and Forecast.

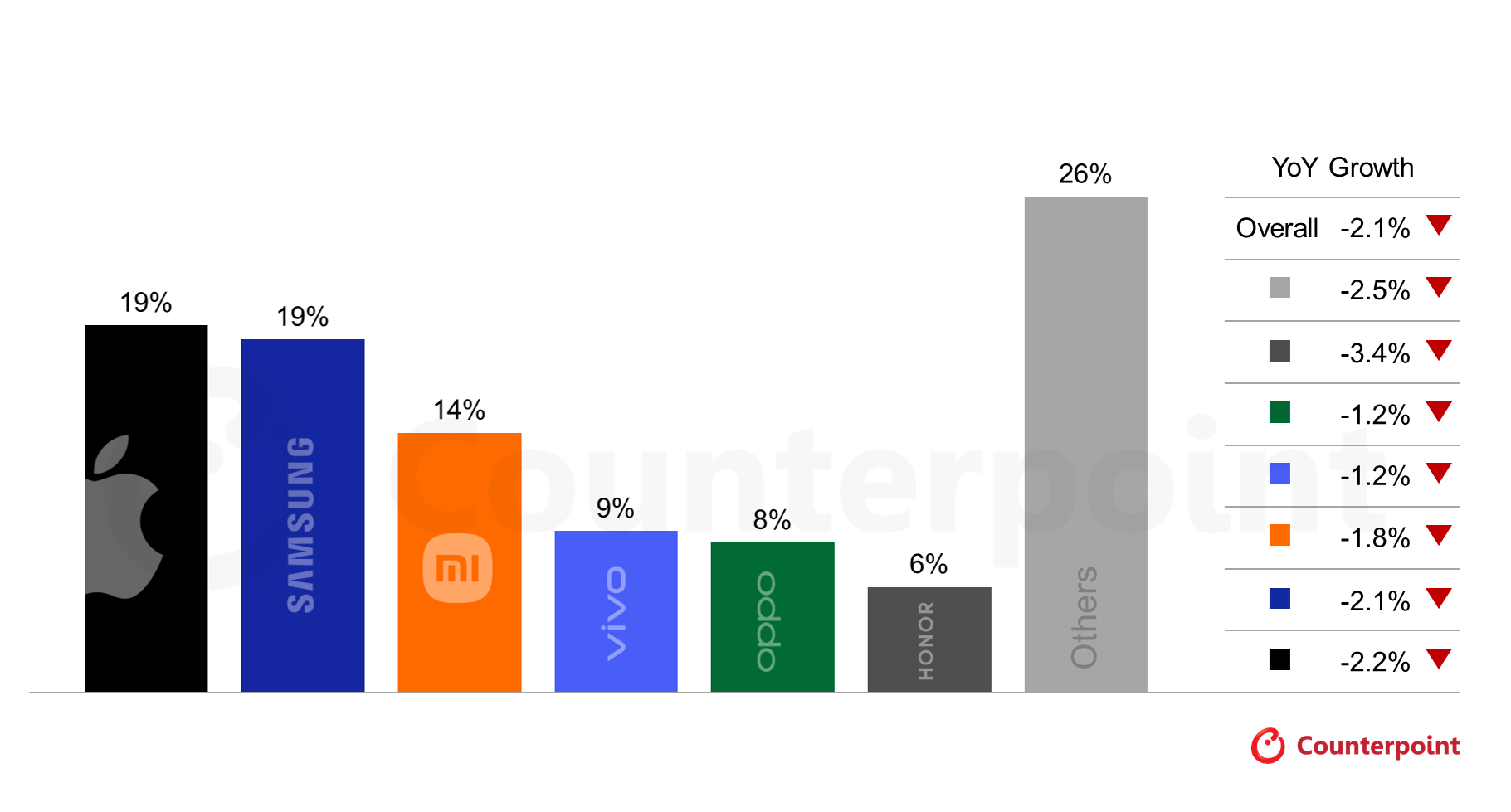

Global Smartphone Market Share and YoY Growth by Key OEM, 2026(E)

Source: Counterpoint Research Global Smartphone Shipment Tracker and Forecast, Dec 2025 Update.

Note: Figures may not add up to 100% due to rounding

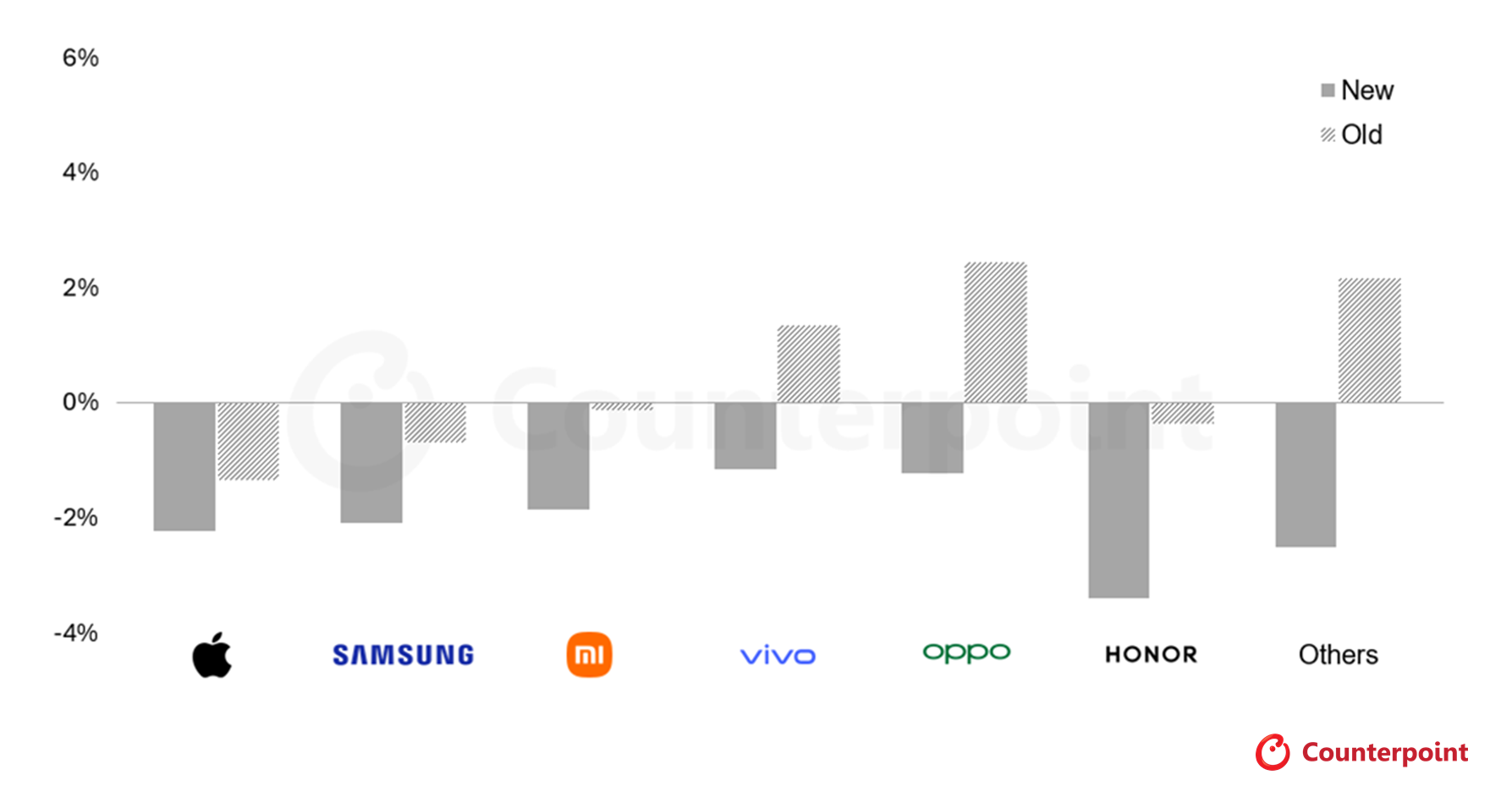

This 2.1% decline translates into a 2.6%pt downward revision in our 2026 forecast, with key Chinese OEMs like HONOR, OPPO and vivo seeing the biggest deltas from previous estimates.

Smartphone Shipment YoY Growth Forecasts and Revisions, 2026

Source: Counterpoint Research Global Smartphone Shipment Tracker and Forecast

Note: New forecast Dec 2025, old forecast Nov 2025

“What we are seeing now is the low end of the market (below $200) being impacted most severely, with BoM (bill of materials) costs increasing by 20%-30% since the beginning of the year,” said Research Director MS Hwang. “The market’s mid- and high-end segments have seen 10%-15% price increases.”

According to Counterpoint Research’s latest ‘Memory Solutions for GenAI’, memory prices could rise another 40% through Q2 2026, resulting in BoM costs increasing anywhere between 8% and over 15% above current elevated levels.

“In the lower price bands, steep price increases on smartphones are not sustainable,” said Senior Analyst Yang Wang. “And if cost pass-through isn’t possible, OEMs will start pruning parts of their portfolios – that’s actually what we are starting to see with significantly reduced volumes of low-end SKUs.”

As a result of cost pass-through and portfolio restructuring, we expect average selling prices (ASPs) to also increase next year by 6.9%, revised up from 3.9% in our previous ASP forecast released in September 2025.

Smartphone makers best positioned to weather supply shortages will be those with scale, broad product portfolios (especially at the high end) and tight vertical integration.

“Apple and Samsung are best positioned to weather the next few quarters,” continued Wang. “But it will be tough for others that don’t have as much wiggle room to manage market share versus profit margins. We will see this play out especially with the Chinese OEMs as the year progresses.”

For these players, we are seeing mitigation strategies, like downgrades of other specifications, being increasingly deployed in the past few months. “In some models, we are seeing downgrades of components like camera modules and periscope solutions, displays, audio components and, of course, memory configurations,” said Senior Analyst Shenghao Bai. “Other tactics include reusing old components, streamlining the portfolio, and pushing consumers to higher-specification ‘Pro’ variants and adopting new designs to stimulate upgrades.”

{kind=link}